South Korea financial literacy event

By Randell Tiongson on August 20th, 2014Annyeonghaseyo!

Catch me for a financial literacy event in Seoul, South Korea this September 7, 2014!

For inquiries, please contact Marlon Albao at albao.marlon@gmail.com

Annyeonghaseyo!

Catch me for a financial literacy event in Seoul, South Korea this September 7, 2014!

For inquiries, please contact Marlon Albao at albao.marlon@gmail.com

I have been busy going to different places to speak to our OFWs and teach them financial education. Although this is a tiring task and despite what other think, traveling all over teaching people is not as glamorous as what others think. There are times that I want to decline invitations already because it takes out a lot of time for me but I never decline because I know that the little I do impacts our OFWs. Studies shows that the OFWs today are saving and investing more than before which is a great development. I also noticed that OFWs respond to financial education more positively and quicker than those in the Philippines. More and more reason why OFW Financial Education is an important advocacy for me and many others.

The growth in the financial literacy for OFWs is largely because of the efforts of many OFWs who are financial educators themselves. My work is such a blessing because I get to have more and more OFW friends who are finance advocates themselves… they have become heroes amidst other heroes.

I am honored to be featuring an article written by a good friend, Rex Holgado — an OFW in Singapore. Rex is one of the most active OFWs in Singapore in financial education and has been instrumental in the amazing growth in financial literacy among Filipinos in Singapore. It is because of OFWs like Rex that there is much hope for the OFWs of the future. I am looking forward standing as a Ninong in his wedding in the not so distant future.

I will be posting may of their articles soon in this website.

———————

OFWs and their Financial Future

by Rex Holgado

Yo friends ‘zup? I assume a lot you do not know me yet, so allow me to shortly introduce myself first. I am an OFW based here in Singapore for over 6 years now. I came here hoping for a greener pasture and help my family back home. And I guess majority, if not all, of the 10 to 13 million overseas Filipino workers (OFWs) around the world have the same reason as mine.

Yo friends ‘zup? I assume a lot you do not know me yet, so allow me to shortly introduce myself first. I am an OFW based here in Singapore for over 6 years now. I came here hoping for a greener pasture and help my family back home. And I guess majority, if not all, of the 10 to 13 million overseas Filipino workers (OFWs) around the world have the same reason as mine.

But do OFWs really able to improve their lives after their stint abroad?

The Past: Financial Trouble

OFWs leave their families and loved ones to look for better opportunities abroad to make their lives better. But more than 2 years ago, Social Enterprise Development Partnerships Inc. (SEDPI), a microfinance non-governmental organization in the Philippines, revealed in a study that 10% of OFWs end up broke even after years of working abroad. And the same study also showed that most or around 80% of Filipinos working abroad overspent and did not really have enough savings.

“Ate Rose”, a house help for 2 years in Kuwait said, “At first I really wasn’t able to save because there were a lot of debts to pay to in the Philippines and I don’t really earn enough to get through it.” But then I asked, “What if you will get a pay increase do you think you can then able to save?” She then replied, “Actually, I don’t know… My expenses seem already hard-wired with my income, if my income increases same goes with my expenses. At some point when I was able to save a small amount of money I tried my luck in networking business hoping to earn extra. So far ayun, hanggang ngayon wala paring extrang kita.”

Ate Rose and her husband do not have a healthcare and insurance, they have two children and currently in high school. Her husband is a full time house husband to take care of the kids. As much as I don’t want this to sound as morbid as you all might think but what if there’s something happened to Ate Rose and she passed away? Oh, my heart aches.

“John”, a technical professional for 3 years in Dubai said, “I have a very small amount of savings but currently no investments because around 80% of my income already goes to loan payments.” I asked, “Can you live with the rest of 20%? What are those loans for?” “My wife helps me with the family expenses. My loans are for the construction of our house.” he replied.

John and his wife are both insured though but they don’t have any investments, no emergency fund and no healthcare other than what the company currently provides. They have one 3-year old kid. And what if John or his wife get retrenched/lose their jobs? Can they tell their child, “Baby, huwag ka muna kumain kasi wala pang trabaho si papa/mama ha? Oh, my heart aches again.

Last month, I’ve been in a Personal Finance seminar of a Christian group’s outreach program for OFWs here in Singapore. I found out that out of the entire crowd of around 80 people (where around half are professionals), only 3 have savings that can sustain their 3-month worth of monthly expenses, only 1 invests—in real estate, no one from them invests in pooled funds nor in stocks. Nobody talk about money or family’s finance in their households or by any mode of communication—unless they are already in a bad situation. But there’s one individual who’ve said she is confident enough that she won’t depend on anyone once she retire. Large part of their income goes to remittances and their remittances do not contain any amount for savings & investments. When I asked who among them have debts, majority of them raised their hands and said, “Kami!” And believe me, everyone were still able to bursts into laughter even they are aware they’re debt-ridden. I confess, I laughed too. Why not?! Laughter is said to be the best medicine. And that time we thought maybe after we laughed all people’s debts will get paid! But you wouldn’t like how our happy faces changed into after realizing that those debts will not ever get paid by mere laughing. Oh here are the sad faces again… So again, if your sickness is borrowing money ‘till you get into financial trouble, laughter can really help to ease the pain but it is not really the cure.

Kidding aside, OFWs might have their own reasons why they were not or cannot able to save. But if we would take a look deeper at those reasons and find their root causes, it would all surely end up with financial literacy and core values.

The Present: Financial Literacy

Six years in abroad I have witnessed a lot, if not enough, how most OFWs struggled in their finances and have seen how they have wasted their hard earned money into unnecessary expenses and worse into the hands of opportunists or those people with no moral compunction. So I joined in the advocacy of financial literacy to help Filipinos, especially OFWs, to get out of the financial pitfall I once got almost trapped too.

Two weeks ago, I was invited to do a personal finance talk in one of our friends’ friend’s house and there was someone who asked that if he would invest in Mutual Funds how much will he get after. Do you see what the usual problem is? Most of us, not just OFWs but all Filipinos especially those who are new to investing, always ask for the “how much would I get” question. Guess why a lot of Filipinos still get scammed?

Here’s a short thought for OFWs out there to not get into bigger financial trouble, “There’s no shortcut to financial freedom.” None that I know of that would work for everyone of us. So go and reflect back on your ultimate goal—to make your and your family’s life better. Save. Do your due diligence and understand very well your investment options. Invest in investment vehicle that would fit your goal. Communicate with your family to discuss and plan well family’s financial matters. And never forget that money is just an instrument to make your goal(s) happen. Never forget that your family, your relationships, and your future are still what really matter most. Be clear with your core values and use them to have a happier, healthier, and wealthier life.

While I have observed that a lot of OFWs are now getting into something they believe they could make their money grow, here are what our financial experts and advocates can say about some financial instruments that OFWs could choose from to invest in for their brighter future:

1. Mutual Funds: “Investing in mutual funds is the easiest way to participate and earn in our country’s economic miracle. Your investments are being professionally managed while you still can attend on things like your work as an OFW and the thing that matters most—your family life.” —Alfonso Gonzales, Mutual Fund Investing Advocate, Mutual Fund investor for almost 16 years

While it is true that this could be one of the best instruments to grow our money still many of us, including OFWs, are still afraid to get into the stock market. But what can a financial expert tell us about it:

2. Stock Market: “The Stock Market is now in a position that it is now available for anyone and everyone who would want to use it as a tool to gain financial freedom. The stock market is one of the greatest equalizers to give the Filipino a fighting chance to be financially free. Do not be scared to brave the unknown. Study. Study. Study. And when you have developed your own winning strategy and conviction you can ride and trade the markets and win not just now but for the long term. My desire for you is to prosper and use money as a tool that it works so hard for you and become financially free. —Marvin Germo, RFP

Some of the OFWs might like to get into business but according to a statistics 50% of businesses might fail in the first year and 90-95% might fail within 5 years. So here’s a simple advice from a very successful entrepreneur:

3. Entrepreneurship: “Anybody can have the mindset of an entrepreneur, but not all can be entrepreneur. OFWs can try entrepreneurship but it is also important that they have the knowledge, passion, right mindset and attitude to become a champion entrepreneur. ” —Paulo Tibig, Entrepreneur and Entrepreneurship Advocate

I and my friends in the advocacy of financial literacy are now stepping up to help more OFWs understand what they are getting into. Instead of falling prey by those who would like to take their hard earned money and lack of financial education for granted.

OFWs Financial Future

If we take a look in Consumer Expectation Survey of Bangko Sentral ng Pilipinas (BSP), we will see that there was a consistent uptrend in OFW allotments in “savings” since 2007 to 2010 but the problem is there was also a consistent uptrend in OFW allotments in “consumer durables” like: gadgets/consumer electronics, appliances, furnitures, & the like, we know that these are not our basic needs—and this could be one of the reasons why less OFWs were really able to save. If OFWs would really understand the importance of saving, they won’t get into this financial pitfall.

Lo and behold! OFW households’ allotments in savings and investments increased in the latest report of Consumer Expectation Survey of BSP. OFW households’ allotments in savings and investments have not just increased but reached the all time high in annual average and in the average of the first two quarters of each year since 2007. 46% of OFW households now have allotments for savings and 8.55% have allotments in investments. OFWs are responding to financial literacy. I believe OFWs are now getting the right financial education. I just hope we can able to sustain this for long term and decrease the numbers of OFWs going back broke.

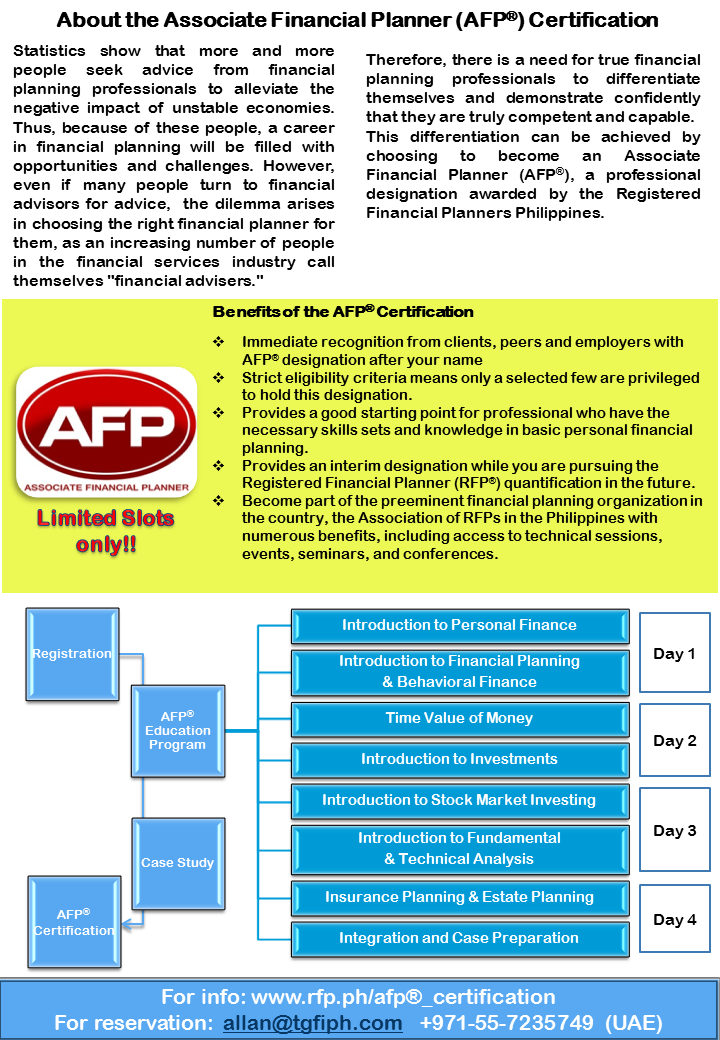

If you are an OFW based in UAE and serious about a fruitful career in the financial services or you are an OFW really serious about understanding financial planning, join us and be certified!

If you are an OFW based in UAE and serious about a fruitful career in the financial services or you are an OFW really serious about understanding financial planning, join us and be certified!

This is a rare opportunity for OFWs to be an expert in financial planning. The program is comprehensive and tackles nearly all pertinent issues in personal finance — from Money Management to Investing.

For inquiries and registration, please email allanmm13@gmail.com or allan@tgfiph.com

…….

MODERATORS:

MODERATORS:

Copyright © 2026 by Randell Tiongson | SEO by SEO-Hacker. Designed, managed and optimized by Sean Si